- Product

- Solutions

- Customers

- Partners

- Resources

- Company

IoT Still Holds Plenty of Promise for Operators

This guest post by Tom Rebbeck of Analysys Mason explores the activities of telecoms operators in IoT and how they can make more of this opportunity. It is based on his recent report, “Rebalancing the Economics of IoT” that was sponsored by MATRIXX and is available here.

Telecoms operators have done well with IoT on many measures. Globally, hundreds of millions of devices are connected using mobile operator networks. IoT is generating USD1 billion or more for the large operators like AT&T, China Mobile and Vodafone.

Despite this, among telecoms operators and in the broader technology community, there remains a perception that IoT has not fulfilled its potential and is growing more slowly than had been anticipated.

Early expectations for IoT were so high that perhaps they were never likely to be realised. Forecasts that more than 10% of operator revenue would come from IoT were never realistic. Even so, IoT may be underperforming against even more modest goals.

IoT Requires Operators to Balance High Connection Volumes with Low Revenue

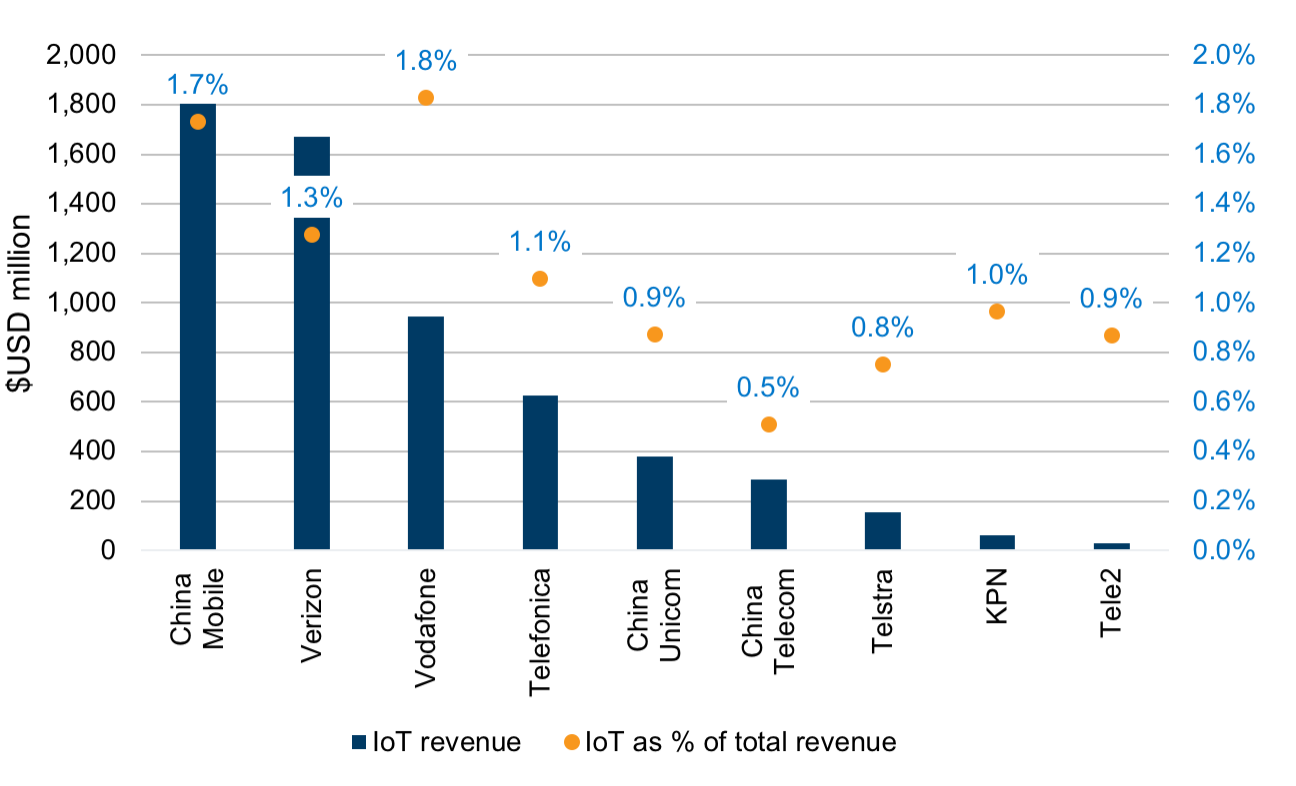

For the nine operators that regularly report data, IoT accounted for just 1.3% of total revenue. Moreover, the operators that publish IoT revenue figures probably have larger IoT businesses than most; for a typical mobile operator, IoT revenue almost certainly equates to less than 1% of total revenue.

Connection numbers are more promising. For certain operators, especially those in China and some high-income countries, IoT already represents a high share of the total connections base. For ten of the operators that report IoT connection numbers, more than 20% of their total connections are for IoT.

The gap between high IoT connection numbers and low revenue highlights a challenge. Smartphones often generate USD20 a month, while most IoT devices generate less than USD2. A different model is needed for IoT. Operators have long recognised this need but it remains only partially addressed. I will explore some of the possible solutions in a future post.

IoT Still Holds Plenty of Promise for Telecoms Operators

IoT continues to be central to the growth plans of many operators. IoT revenue growth is strong, above 20% year on year for many operators. Connectivity is key to IoT products, giving operators a strong claim to an important role. IoT is also an important element of the 5G story for many operators. The most interesting capabilities of 5G (e.g., lower latency, higher reliability) are well suited to supporting new use cases such as connected robots in factories. Many major operators, such as Axiata, Telefónica and Verizon continue to emphasise their IoT activities to investors.

Technology developments should also help to increase the adoption of IoT connectivity. Over time, eSIM and iSIM should reduce costs and complexity, and increase flexibility for customers. They should also help to resolve some of the hardware issues that affect IoT solutions which use cellular connectivity.

The signs for low powered wide area network technologies such as NB-IoT, LTE-M and LoRa, are promising, even if they have taken longer to mature than hoped. Supply-side issues are being resolved — hardware is getting cheaper and becoming more power-efficient. Over 100 established operators have commercial, operational LPWA networks. International roaming agreements are increasingly common.

Demand is also picking up. Contracts with a million or more connections using LPWA technology have been won by Orange (France), Mobily (Saudi Arabia), Telia (Sweden) and Vodafone (Italy). All three Chinese operators have massive NB-IoT networks supporting large contracts.

Another problem, of low awareness, is also reducing: with even relatively small companies developing consumer IoT products.

Finally, while the impact of early 5G launches on IoT will be limited, future releases of 5G will offer different capabilities – low latencies, higher reliability and the ability to support more simultaneous connections — which will open up new possibilities. Exploiting these 5G opportunities will require operator resources, which may not be possible if IoT teams are still locked in extensive negotiations for standard 4G connectivity contracts.

As we will explore in the next post, operators need to find better ways to sell, provision and manage basic IoT connectivity to remain competitive and protect margins, but also to free up resources to make the most of these emerging opportunities.

- Solutions